Featured Articles

Tax Tips

QuickBooks Tips

Any accounting, business or tax advice contained in this communication, including attachments and enclosures, is not intended as a thorough, in-depth analysis of specific issues, nor a substitute for a formal opinion, nor is it sufficient to avoid tax-related penalties. If desired, we would be pleased to perform the requisite research and provide you with a detailed written analysis. Such an engagement may be the subject of a separate engagement letter that would define the scope and limits of the desired consultation services.

- Memorized, Commented, and Scheduled Reports

Tax Return Tips for Last-minute Filers

When it comes to working on your taxes, earlier is better, but many people find preparing their tax return stressful and frustrating and wait until the last minute. If you've been procrastinating on filing your tax return this year, here are eight tips that might help.

Don't Delay

Resist the temptation to put off your taxes until the last minute. Your haste to meet the filing deadline may cause you to overlook potential sources of tax savings and will likely increase your risk of making an error. Getting a head start (even if it is a week or two) will keep the process calm and mean you get your return faster by avoiding the last-minute rush.

Gather Tax Documents in Advance

Make sure you have all the records you need, including W-2s and 1099s. Don't forget to save a copy for your files. If you're missing important tax documents, see What To Do If You're Missing Important Tax Documents below.

Double-check Math and Verify Social Security Numbers

These are among the most common errors found on tax returns. Taking care will reduce your chance of hearing from the IRS. Submitting an error-free return will also speed up your tax refund.

E-file for a Faster Tax Refund

Taxpayers who e-file and choose direct deposit for their refunds, for example, will get their refunds in as few as ten days. That compares to approximately six weeks for people who file a paper return and get a traditional paper check.

Don't Panic if You Can't Pay

If you can't immediately pay the taxes you owe, consider some stress-reducing alternatives. You can apply for an IRS installment agreement suggesting your monthly payment amount and due date and get a reduced late payment penalty rate. You also have various options for charging your balance on a credit card. There is no IRS fee for credit card payments, but the processing companies charge a convenience fee. Electronic filers with a balance due can file early and authorize the government's financial agent to take the money directly from their checking or savings account on the April due date, with no fee.

Request an Extension of Time to File

If the clock runs out, you can get an automatic six-month extension bringing the filing date to October 17, 2022 - but make sure you pay by the April 18 due date. However, the extension does not give you more time to pay any tax due. You will owe interest on any amount not paid by the April deadline, plus a late payment penalty if you have not paid at least 90 percent of your total tax by that date.

Taxpayers Outside the United States File June 15

U.S. citizens and resident aliens who live and work outside the U.S. and Puerto Rico have until June 15, 2022, to file their 2021 tax returns and pay any tax due. The June 15 deadline also applies to military members on duty outside the U.S. and Puerto Rico who do not qualify for the longer combat zone extension. Affected taxpayers should attach a statement to their return explaining which of these situations apply. Although taxpayers abroad get more time to pay, interest - currently at the rate of 3% per year, compounded daily - applies to any payment received after this year's April 18 deadline.

Military Service Members Serving in a Combat Zone

Combat zone taxpayers (including eligible support personnel) have at least 180 days after they leave the combat zone to file their tax returns and pay any tax due - including those serving in Iraq, Afghanistan, and other combat zones. A complete list of designated combat zone localities is available on the IRS website. Combat zone extensions also give affected taxpayers more time for various other tax-related actions, including contributing to an IRA. Various circumstances affect the exact length of the extension available to taxpayers.

Help is Just a Phone Call Away

If you run into any problems, have any questions, or need to file an extension, contact the office today.

Cash Management Tips for Your Small Business

Cash flow is the lifeblood of every small business but many business owners underestimate just how vital managing cash flow is to their business's success. In fact, a healthy cash flow is more important than your business's ability to deliver its goods and services.

While that might seem counterintuitive, consider this: if you fail to satisfy a customer and lose that customer's business, you can always work harder to please the next customer. If you fail to have enough cash to pay your suppliers, creditors, or employees, you are out of business.

What is Cash Flow?

Cash flow, simply defined, is the movement of money in and out of your business; these movements are called inflow and outflow. Inflows for your business primarily come from the sale of goods or services to your customers but keep in mind that inflow only occurs when you make a cash sale or collect on receivables. It is the cash that counts! Other examples of cash inflows are borrowed funds, income derived from sales of assets, and investment income from interest.

Outflows for your business are generally the result of paying expenses. Examples of cash outflows include paying employee wages, purchasing inventory or raw materials, purchasing fixed assets, operating costs, paying back loans, and paying taxes.

A tax and accounting professional is the best person to help you learn how your cash flow statement works. He or she can prepare your cash flow statement and explain where the numbers come from. If you need help, don't hesitate to call.

Cash Flow versus Profit

While they might seem similar, profit and cash flow are two entirely different concepts, each with entirely different results. The concept of profit is somewhat broad and only looks at income and expenses over a certain period, say a fiscal quarter. Profit is a useful figure for calculating your taxes and reporting to the IRS.

Cash flow, on the other hand, is a more dynamic tool focusing on the day-to-day operations of a business owner. It is concerned with the movement of money in and out of a business. But more important, it is concerned with the times at which the movement of the money takes place.

In theory, even profitable companies can go bankrupt. It would take a lot of negligence and total disregard for cash flow, but it is possible. Consider how the difference between profit and cash flow relate to your business.

If your retail business bought a $1,000 item and turned around to sell it for $2,000, then you have made a $1,000 profit. But what if the buyer of the item is slow to pay his or her bill, and six months pass before you collect on the account? Your retail business may still show a profit, but what about the bills it has to pay during that six-month period? You may not have the cash to pay the bills despite the profits you earned on the sale. Furthermore, this cash flow gap may cause you to miss other profit opportunities, damage your credit rating, and force you to take out loans and create debt. If this mistake is repeated enough times, you may go bankrupt.

Analyzing Your Cash Flow

The sooner you learn how to manage your cash flow, the better your chances of survival. Furthermore, you will be able to protect your company's short-term reputation as well as position it for long-term success.

The first step toward taking control of your company's cash flow is to analyze the components that affect the timing of your cash inflows and outflows. A thorough analysis of these components will reveal problem areas that lead to cash flow gaps in your business. Narrowing, or even closing, these gaps is the key to cash flow management.

Some of the most important components to examine are:

- Accounts receivable. Accounts receivable represent sales that have not yet been collected in the form of cash. An accounts receivable balance sheet is created when you sell something to a customer in return for his or her promise to pay at a later date. The longer it takes for your customers to pay on their accounts, the more negative the effect on your cash flow.

- Credit terms. Credit terms are the time limits you set for your customers' promise to pay for their purchases. Credit terms affect the timing of your cash inflows. A simple way to improve cash flow is to get customers to pay their bills more quickly.

- Credit policy. A credit policy is the blueprint you use when deciding to extend credit to a customer. The correct credit policy - neither too strict nor too generous - is crucial for a healthy cash flow.

- Inventory. Inventory describes the extra merchandise or supplies your business keeps on hand to meet the demands of customers. An excessive amount of inventory hurts your cash flow by using up money that could be used for other cash outflows. Too many business owners buy inventory based on hopes and dreams instead of what they can realistically sell. Keep your inventory as low as possible.

- Accounts payable and cash flow. Accounts payable are amounts you owe to your suppliers that are payable at some point in the near future - "near" meaning 30 to 90 days. Without payables and trade credit, you'd have to pay for all goods and services at the time you purchase them. For optimum cash flow management, examine your payables schedule.

Some cash flow gaps are created intentionally. For example, a business may purchase extra inventory to take advantage of quantity discounts, accelerate cash outflows to take advantage of significant trade discounts or spend extra cash to expand its line of business.

For other businesses, cash flow gaps are unavoidable. Take, for example, a company that experiences seasonal fluctuations in its line of business. This business may normally have cash flow gaps during its slow season and then later fill the gaps with cash surpluses from the peak part of its season. Cash flow gaps are often filled by external financing sources. Revolving lines of credit, bank loans, and trade credit are just a few of the external financing options available that you may want to discuss with us.

Monitoring and managing your cash flow is important for the vitality of your business. The first signs of financial woe appear in your cash flow statement, giving you time to recognize a forthcoming problem and plan a strategy to deal with it. Furthermore, with periodic cash flow analysis, you can head off those unpleasant financial glitches by recognizing which aspects of your business have the potential to cause cash flow gaps.

Make Sure Your Business has Adequate Funds

If you need help covering day-to-day expenses or analyzing and managing your cash flow more effectively, please call the office today.

File on Time Even if You Can’t Pay

Generally, taxpayers should file their tax returns by the deadline even if they cannot pay the total amount due, but if you can't, there are several options. Let's take a look at a few scenarios:

1. An individual taxpayer owes taxes but can't pay in full by the deadline. If this is the case, file a tax return or request an extension of time to file by the April 18 deadline. If tax is owed and a return is not filed on time - or an extension is not requested - the taxpayer may face a failure-to-file penalty for not filing on time.

2. File an extension. Taxpayers should remember that an extension of time to file is not an extension of time to pay. An extension gives taxpayers until October 17, 2022, to file their 2021 tax return, but taxes owed are still due April 18, 2022 (April 19 if you live in Maine or Massachusetts).

To file an extension, taxpayers must do one of the following:

- File Form 4868, Application for Automatic Extension of Time, through their tax professional

- Submit an electronic payment with Direct Pay, Electronic Federal Tax Payment System or by debit, credit card or digital wallet and select Form 4868 or extension as the payment type.

3. Set up a payment plan as soon as possible. Taxpayers who owe money but cannot pay in full by April 18 (April 19 if you live in Maine or Massachusetts) don't have to wait for a tax bill to set up a payment plan. Instead, they can:

- Apply for a payment plan on IRS.gov; or

- Submit a payment plan request using Form 9465, Installment Agreement Request

4. Pay as much as possible by the April 18 (or 19) due date. Whether filing a return or requesting an extension, taxpayers must pay their tax bill in full by the May deadline to avoid interest and penalties. People who do not pay their taxes on time will face a failure-to-pay penalty. The IRS has options for taxpayers who can't afford to pay taxes they owe.

Don't wait. If you need assistance filing a tax or an extension for 2021, please call the office as soon as possible.

What To Do if You’re Missing Important Tax Documents

As the April 18th tax deadline quickly approaches, last-minute tax filers should make sure they have all their documents before filing a tax return. You should have received a Form W-2, Wage and Tax Statement, from each of your employers for use in preparing your federal tax return. Employers must furnish this record of 2021 earnings and withheld taxes no later than January 31, 2022. As such, most taxpayers should have received their documents near the end of January, including:

- Forms W-2, Wage and Tax Statement

- Form 1099-MISC, Miscellaneous Income

- Form 1099-INT, Interest Income

- Form 1099-NEC, Nonemployee Compensation

- Form 1099-G, Certain Government Payments; like unemployment compensation or state tax refund

Taxpayers who haven't received a W-2 or Form 1099 should contact the employer, payer, or issuing agency and request the missing documents. This also applies to those who received an incorrect W-2 or Form 1099.

If they can't get the forms, they must still file their tax return on time or get an extension to file. To avoid filing an incomplete or amended return, they may need to use Form 4852, Substitute for Form W-2, Wage and Tax Statement or Form 1099-R, Distributions From Pensions, Annuities, Retirement or Profit-Sharing Plans, IRAs, Insurance Contracts, Etc.

If a taxpayer doesn't receive the missing or corrected form in time to file their tax return, they can estimate the wages or payments made to them and any taxes withheld. They can use Form 4852 to report this information on their federal tax return.

If they receive the missing or corrected Form W-2 or Form 1099-R after filing their return and the information differs from their previous estimate, they must file Form 1040-X, Amended U.S. Individual Income Tax Return.

Incorrect Form 1099-G for unemployment benefits

Many people received unemployment compensation in 2021. Unemployment compensation is taxable and must be reported on the recipient's tax return.

Taxpayers who receive an incorrect Form 1099-G, Certain Government Payments (Info Copy Only), for unemployment benefits they did not get should contact the issuing state agency to request a revised Form 1099-G showing their correct benefits. Taxpayers who are unable to obtain a timely, corrected form from states should still file an accurate tax return, reporting only the income they did receive.

Filing an Amended Return

If you receive a corrected W-2 or 1099 after your return is filed and the information it contains does not match the income or withheld tax that you reported on your return, you must file an amended return on Form 1040X, Amended U.S. Individual Income Tax Return.

Don't Wait, Take Action Now

If you're missing important tax forms, please contact the office for assistance.

Memorized, Commented, and Scheduled Reports

QuickBooks reports are your reward for conscientiously tracking your business income and expenses. Rather than scanning through lists of customer invoices to see which ones are past due, you can run an A/R Aging report with a couple of clicks. Same goes for your bills: A/P Aging. Need to know what items are selling well and which are not? Run Inventory Stock Status by Item.

The insight reports can give you don’t just tell you how many products you’ve sold and what you owe and who owes you. They help you make better business decisions and plan for the future.

But you can do much more with them than just absorb their information and move on with your day. You can modify them, share them and make comments on individual line items. Here’s how. (You can work with a QuickBooks sample file for most of these steps. Go to File | Open Previous Company.)

Memorizing Reports

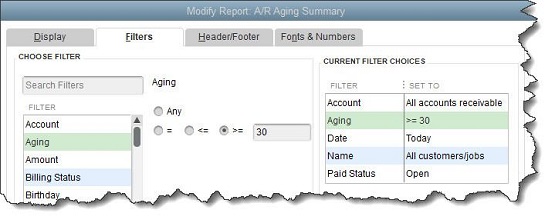

Where does QuickBooks start when you create a report? How does it know, for example, what date range you want the report to cover and what customers and vendors, and items should be included? It doesn’t. The pre-built reports that QuickBooks can create have default settings. That is, they just provide a starting place. To run the reports with the content you want to see, you have to modify them by clicking the Customize Report button in the upper left and specifying your preferences.

Figure 1: You can change numerous settings in QuickBooks’ reports, and then memorize those preferences for use again.

Once you’ve modified a report that you want to save, it’s easy to keep a copy of it with its new settings. With the report open, click the Memorize button at the top of the screen. When the Memorize Report window opens, give your report a Name that you’ll remember and will associate with its settings and content. If you’d like to save it in a Memorized Report Group, check that box and open the drop-down menu to select from the options there ( Company, Customers, etc.).

Do you think other QuickBooks users might want to use the model you created? Click the box next to Share this report template with others. In the window that opens, you’ll need to give your report a Description. You can choose to share your name or post it anonymously.

Click Share, and you’ll be able to see your template in QuickBooks’ Report Center by clicking Shared with the Memorized tab highlighted. Other users will only be able to access the settings and use them with their own data. Yours will not be included.

Commented Reports

Figure 2: You can click the dialogue balloon next to any item and enter a comment about it in the box below.

QuickBooks’ Reports menu is a comprehensive listing of all of your report options. Click on it, and you’ll see that there’s a link for your Memorized reports right at the top. You’ll also see a link for Commented Reports. QuickBooks allows you to enter comments in reports.

To see this in action, open the Sales by Item Detail report. Click Comment on Report at the top of the screen. QuickBooks will open another copy with small dialogue balloons displayed next to every element of the report (Name, Qty, Sales Price, etc.) in every row. Click the one you want to comment on, and a window opens below. Enter your comment.

The number in front of the comment (1) matches the correct location in the report. Click Save over to the right. You can now Print or E-mail the commented report or Save it after giving it a Name. To see the list of reports you’ve entered comments on, open the Reports menu and select Commented Reports. Your original report will not contain the comments, only the commented one you saved.

Scheduling Reports

You may be commenting on reports for your purposes, but you may also want to share them with colleagues or other business contacts sometimes. QuickBooks allows you to email selected reports on a schedule, as long as they’re memorized.

Scheduling reports isn’t such a complex process, but your system has to be set up precisely for it to work. For example, you must:

- Be in single-user mode.

- Have an email service connected to QuickBooks (if it’s Outlook, it must be open and running).

- Not be in sleep or hibernation mode.

- Have QuickBooks updated to the latest release.

- Have QuickBooks running.

Your report data is very sensitive, and emailing it to the wrong person could be disastrous. If you need help with this or any other QuickBooks-related issues, please call, and someone can walk you through this process.